CHAPTER 4 MINE FINANCING IN DIFFICULT TIMES: A REVIEW OF CURRENT GLOBAL TRENDS

| Jurisdiction | United States |

(Apr 1999)

MINE FINANCING IN DIFFICULT TIMES: A REVIEW OF CURRENT GLOBAL TRENDS

J. Michael Armstrong 1

NM Rothschild & Sons Canada Limited

Toronto, Ontario, Canada

1. INTRODUCTION

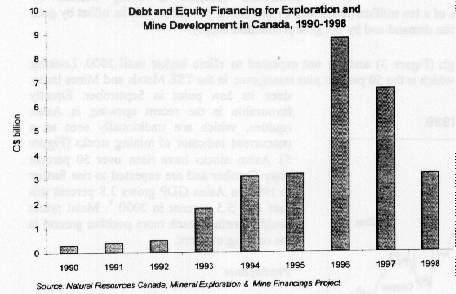

Financing mining projects in the current economic climate is a difficult task, especially for small to mid-size companies. Conventional sources of debt and equity finance have been drying up steadily since 1996 (Figure 1) and now, with the prices of mining stocks near record lows, a credit crunch sending interest rates higher, and plunging metal prices reducing cash flow, mining companies have few funding alternatives. Surprisingly, mining expenditures show few signs of slowing down. World-wide capital spending on mining and milling projects in 1999 is expected to total $50.6 billion2 , up from $48.5 billion in 1998. The number of planned projects has decreased, however, from 140 to 116, indicating a shift towards fewer, larger projects3 . In other words, the larger companies are expanding at the expense of the small to mid-size players. These expenditures, however, are less for new project development than for completing previously started projects. With expenditure increasing and financing on the wane, there is clearly a gap that needs to be closed. The answer will lie in creative financing and this may require either inventing or borrowing new funding techniques from other industries.

Figure 1

This paper begins with an overview of the key drivers of mining industry performance, such as prices, production, exploration and costs. This leads into a discussion of the three broad types of mine financing, internal funds, equity and debt, as well as a review of the major trends in project finance, and concludes with a comparative overview of these sources of financing.

[Page 4-2]

2. MINING INDUSTRY OVERVIEW

Metal Prices

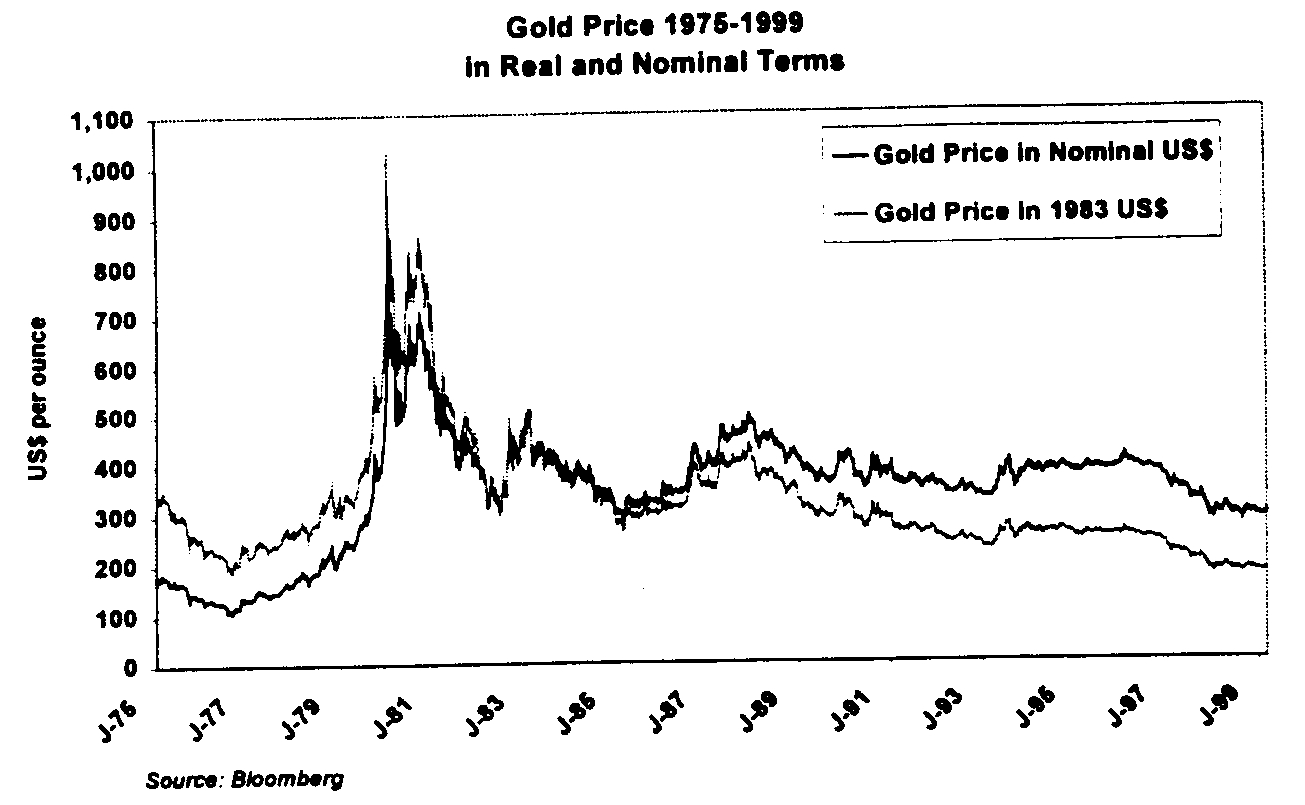

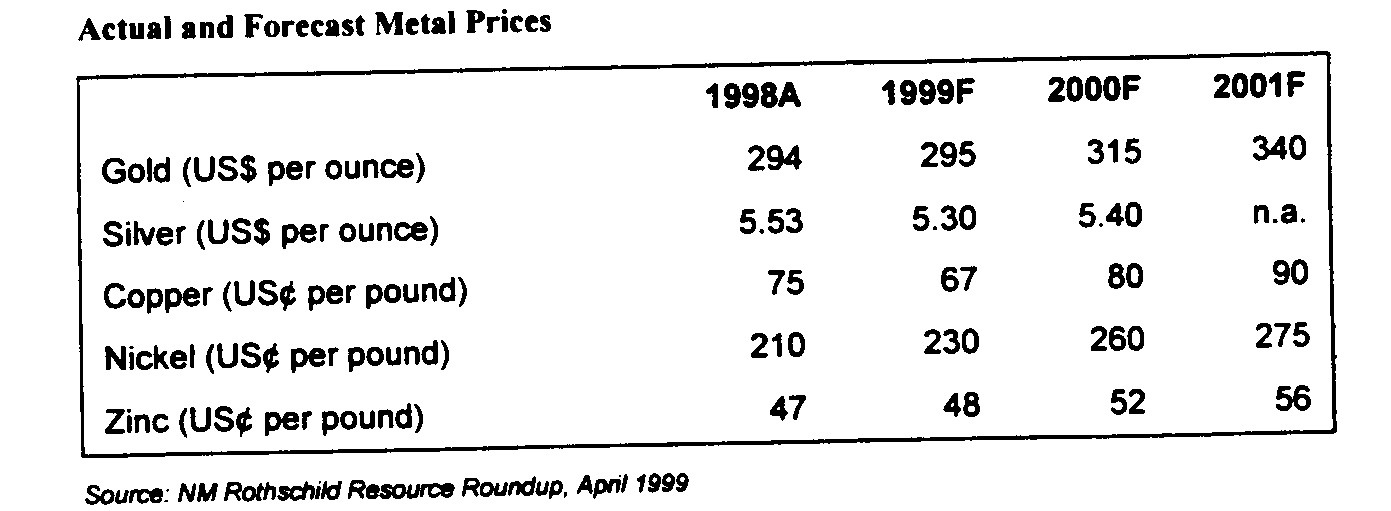

At time of printing, the gold price was trading at approximately $280 to $285 per ounce, near last August's 19-year low of $274 per ounce, having dropped over 30 percent just since early 1996 when prices were over $410 per ounce (Figure 2). However, gold appears to have touched bottom and is expected to rise steadily starting this year (Figure 4) according to various forecasts.

Figure 2

Gold price forecasts are generally based on an analysis of four main drivers of the gold price: central bank bullion activity; investment demand; Asian demand; and production supply. Most analysts forecast a steady rise in the gold price. In the opinion of ABN Amro Bank, for example, the gold price will rise because while downward pressure is being exerted by impending central bank sales (including rumours of a ten million ounce sale by the IMF), this factor will be offset by gold investors building long positions, by renewed Asian demand and by flat gold production supply.4

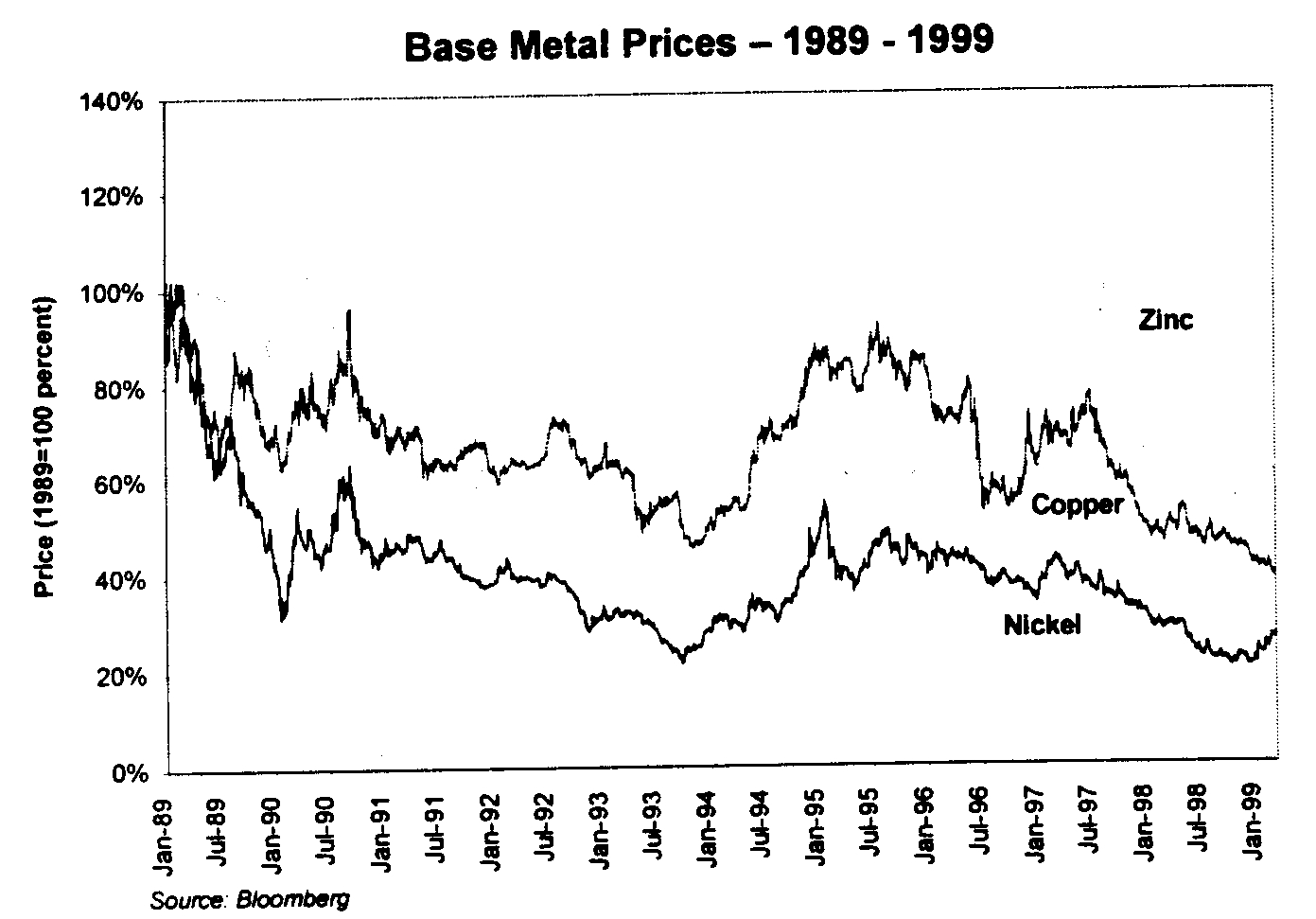

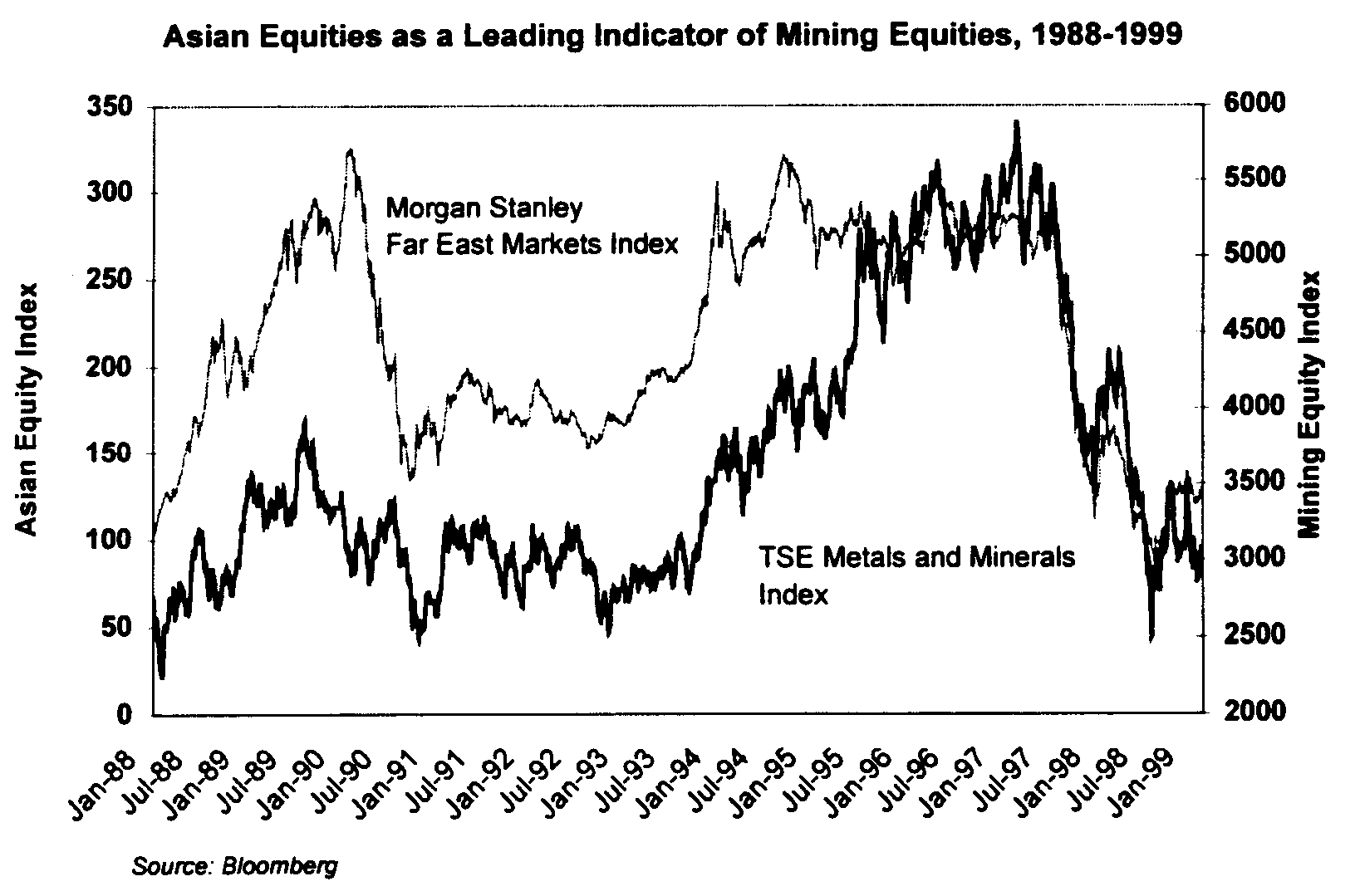

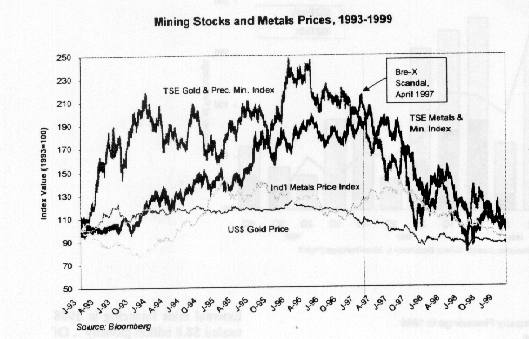

Base metals prices are currently also in a trough (Figure 3) and are not expected to climb higher until 2000. Looking forward, there are signs of recovery, not least of which is the 50 percent plus resurgence in the TSE Metals and Mines Index since its low point in September. Equally favourable is the recent upswing in Asian equities, which are traditionally seen as a concurrent indicator of mining stocks (Figure 5). Asian stocks have risen over 50 percent since October and are expected to rise further in 1999 as Asian GDP grows 3.8 percent this year and 5.5 percent in 20005 . Metal prices could therefore reach more positive ground in the coming quarters.

Figure 3

Production

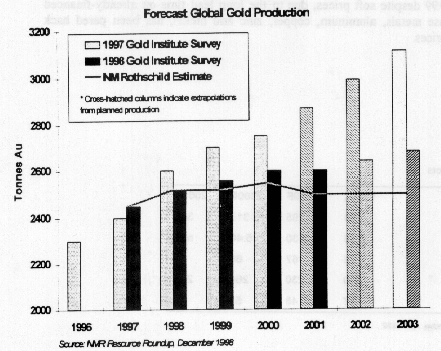

The substantial slump in gold prices has had a significant impact on planned gold production, as producers have shelved several new projects and focussed production on high-grade, low-cost reserves. As a result, The Gold Institute now forecasts gold production growth at only one percent per year for the next four years, down sharply from its 1997 forecast (Figure 6). Production to 2000 is planned to shift towards Australia and South Africa,

[Page 4-3]

aided by their weakening currencies (which drive up the A$ and ZAR gold prices), while growth in North American production will be virtually nil6 .

As for base metals, mine production will rise in 1999 despite soft prices, due to the long lead time on already-financed projects. Smelter production for the four major base metals, aluminum, copper, zinc and nickel, has been pared back slightly, but not enough to stem supply pressure on prices.

Figure 4

Figure 5

[Page 4-4]

Exploration

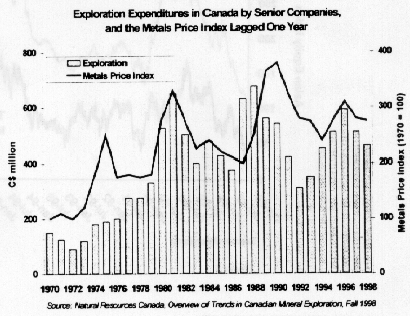

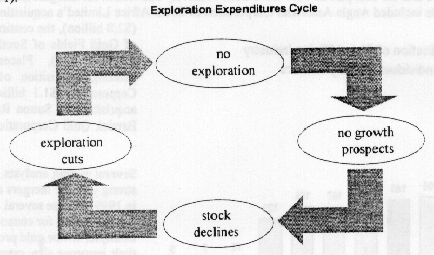

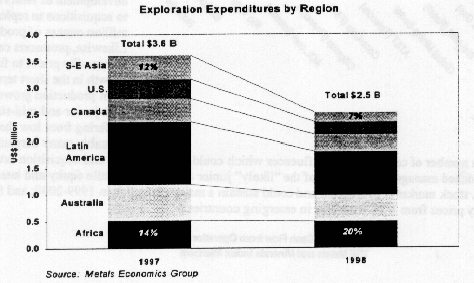

Historically, exploration expenditures have tracked metals prices with a one-year lag, as evidenced by exploration trends in Canada (Figure 7). Global exploration expenditures dropped from 1997 to 1998 and have dropped again in 1999 given the current state of metals prices. Low metal prices have forced senior producers to cut costs, and the first costs to be cut were exploration expenditures. This in turn has reduced the number of joint ventures with junior exploration companies. Exploration budgets have been slashed in order to preserve capital, leading to a vicious downward cycle as illustrated in Figure 8. As exploration budgets are reduced, less exploration is leading to fewer growth prospects, which results in a decrease in share prices. With debt almost never an option for junior companies, joint venture funding squeezed and with the equity markets closed (see "Equity Financing", below), junior companies in particular have few financing sources available. Near term exploration activity will therefore remain low until higher commodity prices return or the expectation of their return is believed. Regionally however, it appears that exploration has shifted proportionally away from South-East Asia and into Africa, with other regions retaining constant shares (Figure 9).

Figure 6

Operating Costs

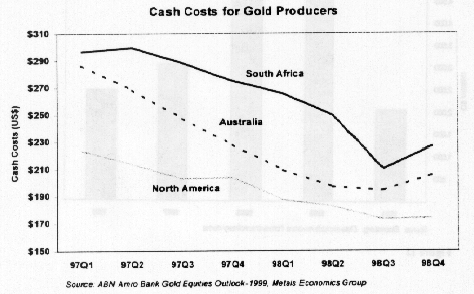

Cash costs of gold production have continued to track the gold price downwards in 1998. These cost reductions have been realised by shifting production to high-grade, low-cost reserves and to some extent by cost-saving technologies, but the greatest contributor has been currency depreciation in non-U.S. countries, particularly Australia and South Africa (Figure 10). In Australia, for instance, U.S. dollar cash costs have dropped 28 percent since January 1997, 20 percent of which is directly related to the weakened Australian dollar. As a result, many Australian companies, for example, are producing gold at better margins now than they were in 1987. Globally, the margin between the gold price and cash costs is narrowing, but is still around $85 per ounce.

Figure 7

Base metal producers have not been as effective in reducing cash costs below metal prices. A significant proportion of producers are losing money, with nickel producers being the hardest hit (Figure 11).

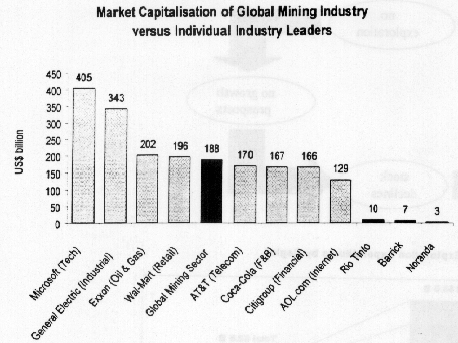

The cumulative effect of low commodity prices, reduced cash flow and thin profits has been a severe decline in mining share prices. At $170

[Page 4-5]

billion, the aggregate market capitalization of the precious and base metals mining industry is now less than the individual market capitalisation of large U.S. multinationals such as: General Electric Company, Microsoft Corporation and Wal-Mart Stores Inc. (Figure 11).

Figure 8

Figure 9

Figure 10

[Page 4-6]

Merger and Acquisition Activities

Contrary to expectations, 1998 and the first part of 1999 have been relatively uneventful for mergers and acquisitions in the mining sector. The larger deals included Anglo American Corporation of South Africa Limited's acquisition of Minorco SA ($2.8 billion), the continued restructuring of Gold Fields of South Africa Limited ($1.5 billion), Placer Dome Inc.'s pending acquisition of Getchell Gold Corporation ($1.1 billion) and pending acquisition of Sutton Resources Ltd. by Barrick Gold Corporation ($320 million)

Figure 11

Several mining analysts are predicting a strong year for mergers and acquisitions in 1999 because several factors are driving a need for consolidation. For example, senior gold producers, due to their immense size, cannot sustain growth purely through internal development of reserves and must look to acquisitions to replenish two to four million ounces of production per year. Likewise, producers cannot rely on commodity prices to fuel earnings growth in the short term, so it must come from production growth. In addition, with junior and mid-sized companies suffering from low share prices, there are arguably many bargains to be had.

However, there are a number of countervailing influences which could subdue merger and acquisition activity in 1999. These include: entrenched management at many of the "likely" junior candidates; volatile equity and interest rate markets; the fear that the U.S. stock market is overheated and could sustain a major correction in 1999-2000; and finally, fallout in share and commodity prices from Y2K problems in emerging countries.

Figure 12

[Page 4-7]

3. INTERNAL FINANCING

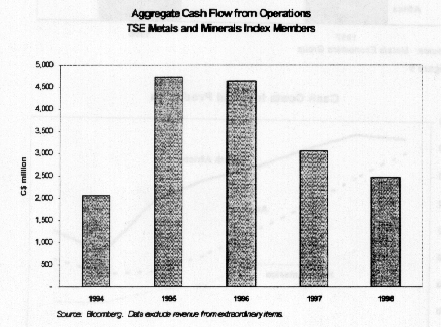

Cash flow from operations is a major source of funding for mining companies, and has been falling and will likely continue to fall through 1999 until metals prices rebound. This is particularly the case for small to mid-size producers (Figure 12). Consequently, other sources of internal funding will have to be tapped. Mining firms have a few options. The most obvious is asset sales.

Figure 13

Asset Sales

Inco Limited for example, sold its nickel alloys business in October, 1998 for $365 million, and floated its interest in Doncasters plc in January, 1997, for $132 million. The proceeds of these transactions were applied towards paying down debt incurred, and buying back shares issued, as part of its August, 1996 acquisition of Diamond Fields Resources Inc. Furthermore, during the past two years, Cyprus Amax Minerals Company has sold its gold business and its lithium business and is in the final stages of selling its coal assets, in an attempt to...

To continue reading

Request your trial