Chapter 3 Market-Approach Valuation Methods

| Jurisdiction | United States |

Chapter 3: Market-Approach Valuation Methods

A. Fundamentals of the Market Approach6

An entrepreneur was having lunch with a friend in the investment banking business. "You know," said the entrepreneur, "I've been talking with some local business people about the possibility of buying Community Convenience Stores. It's a fairly small chain, not publicly traded, and does not appear to be very well-run or responsive to the needs of the region. They think it could be much better managed and more profitable. How much do you think it would take to buy the firm?"

"How much are its current earnings?," asked the financier.

"Around $500,000."

"I don't know much about the company," said the financier, "but generally, convenience stores of that size in the area are selling at around five times current earnings. So $2.5 million might be a ballpark figure."

The entrepreneur's friend was giving a rough estimate of the value of a business based on a multiple of its business financial performance: current net earnings. Pricing multiples of this kind are often used as a rule of thumb for estimating the value of a business.

The value of a company as an ongoing business — and not as a set of separately salable parts — is ultimately determined by its ability to generate a stream of future earnings and cash flow. The greater its ability to expand that stream, the greater its value.

When they buy shares of a company, investors understand that they are not buying the past or the present. They are buying the future. The greater the expectations for future growth in earnings and cash flows, the more the investor is willing to pay. Risk also affects how investors view the value of a company. The greater the uncertainty associated with a firm's expected earnings or cash flow, the less investors are willing to pay for it. Thus, as risk increases, the company's pricing multiple is reduced.

Unfortunately, the use of pricing multiples is not a simple procedure. Pricing multiples vary in their definition and the data used to calculate them. To get a sense of how these different measures are derived from a company's financial statements and used to estimate a company's value, let's consider T&A Fabrications, Inc., a public company described by Exhibit 3-1.

Exhibit 3-1: T&A Fabrications, Inc. Selected Financial Data ($ millions)

| Sales | $10.0 |

| - Cost of Goods Sold | 6.5 |

| = Gross Margin | $3.5 |

| - Selling, General and Administrative | 1.3 |

| - Depreciation | 0.6 |

| - Amortization | 0.1 |

| - Interest | 0.5 |

| = Net Profit Before Taxes | $1.0 |

| - Taxes (40%) | 0.4 |

| = Net Profit After Taxes | $0.6 |

| Other Information | |

| Capital Expenditures | $0.1 |

| Increase in Working Capital | $0.1 |

| Long-Term Debt | $3.0 |

| Total Debt | $5.0 |

| Market Price Per Share ($ per share) | $15.00 |

| Number of Shares Outstanding | 1 million |

The following sections use T&A to describe several pricing multiples that are commonly used in both transactional and legal valuation assignments.

P/E Pricing Multiple

We observe the value that investors place on a company through the multiple they pay for certain measures of business financial performance. One of the most widely used equity pricing multiples is the P/E, or price/earnings multiple. This metric is a ratio of the stock price to the company's current earnings per share, indicating the amount investors are willing to pay for each dollar of current net earnings. For example, a P/E multiple of 10 indicates that investors are paying $10 for each dollar of current net earnings. The size of the pricing multiple reveals investors' expectations for future growth. For example, their willingness to pay $20 or $30 for each dollar of current earnings indicates their expectation with respect to future growth. Evidence confirms that in general, high-growth companies command higher P/E multiples.

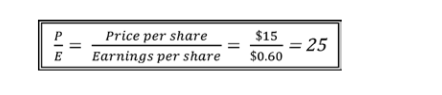

Net earnings are the basis for the P/E calculation. This measure includes the effects of operations, capital structure (namely interest payments) and taxes. Let's consider the P/E multiple for the publicly held company T&A Fabrications described in Exhibit 3-1. The company's net profit after taxes was $600,000 and it has 1 million shares outstanding, indicating earnings per share of $0.60. Thus, the price/earnings multiple can be derived as follows:

Obviously, the same pricing multiple could have been derived by dividing the total market value of T&A's equity, $15 million ($15 per share x 1 million shares), by its total earnings, $0.6 million. The P/E multiple, 25, has a number of potential uses. For example, if the company's earnings are projected to be $1 million five years from now, one might use the pricing multiple to obtain the estimated equity value at that time as $25 million (25 x earnings of $1 million). Clearly, this equity valuation method assumes that the P/E multiple will not change over the five-year interval.

It is important to note that the P/E multiple is used to estimate the value of the company's equity. If the objective is to estimate the total value of the company, the analyst should add the company's long-term, interest-bearing debt to its equity value. Another application of the P/E multiple is the valuation of a privately held firm. Suppose that you want to value the equity of a privately held firm in the same industry as T&A, with reported earnings of $1.5 million. You can use T&A as a surrogate company and multiply the privately held company's $1.5 million earnings by T&A's P/E multiple, 25, to obtain an estimated equity value of $37.5 million, prior to what is referred to as the discount for lack of marketability (or DLOM). This discount accounts for the fact that T&A is a publicly traded company, and the subject company in this example is privately held. Though no two companies are identical in all respects, the use of a surrogate involves the analyst's judgment in the selection of the most appropriate companies to provide pricing guidance.

EBIT Pricing Multiple

To estimate the value of a debtor company, analysts often use a pricing multiple based on the company's earnings before interest and taxes (EBIT). The EBIT is frequently referred to as operating income. The pricing multiple is defined as the total value of the company's invested capital divided by its EBIT. The total value of the company's invested capital is estimated by adding the value of its equity to the value of its long-term, interest-bearing debt. EBIT represents the debtor company's earnings before interest and taxes, which, unlike net income, are the earnings available to both equity holders in the form of profits and to debt-holders to cover the company's fixed financial obligations. Therefore, while the P/E pricing multiple, which is based on net earnings available to shareholders, is used to estimate the value of the company's equity, the EBIT pricing multiple is used to estimate the total invested capital value of the company.

To determine EBIT for the T&A Fabrication example discussed in Exhibit 3-1, the following calculation is performed:

Exhibit 3-2: T&A Fabrications, Inc. EBIT Calculation ($ millions)

| Sales | $10.0 |

| - Cost of Goods Sold | 6.5 |

| - Selling, General and Administrative | 1.3 |

| - Depreciation | 0.6 |

| - Amortization | 0.1 |

| = EBIT | $1.5 |

Given that the company equity is valued at $15 million and that the company has $5 million in outstanding debt, the EBIT pricing multiple can be derived as follows:

Let's suppose that the T&A EBIT in five years is expected to increase to $2.5 million. The estimated total invested capital value of the company five years from now is $33.25 million (i.e., a value-to-EBIT pricing multiple of 13.3 x projected EBIT of $2.5 million). The underlying assumption is that the EBIT multiple will stay stable over the coming five years. If five years from now the debt is projected to be $9 million, the projected market value of equity at that time will be equal to $24.25 million (total invested capital value of $33.25 million - debt of $9 million).

Another application of the EBIT pricing multiple is the estimation at the present time of either the total invested capital value of a privately held company or the value of the company's equity. In these situations, one could calculate the EBIT pricing multiple for a company such as T&A Fabrications and then multiply this value by the EBIT of the privately held company.

For example, by multiplying T&A pricing multiple of 13.3 and the privately held company's EBIT of, say, $4.5 million, one would obtain an estimate of $59.85 million (EBIT multiple of 13.3 x EBIT of $4.5 million) for the value of the subject company. To estimate the value of the privately held company equity, one would subtract the total value of its debt — say, $10 million — from the company's value of $59.85 million, to obtain an estimate of the value of its equity, $49.85 million. Once again, a further downward adjustment may be needed — a discount for lack of marketability — accounting for the fact that unlike T&A, the subject company is privately held.

This valuation method is frequently used in both corporate finance and litigation settings. For example, in a recent fraudulent conveyance matter involving the equity valuation of Great Lakes Bus Lines, the EBIT pricing multiple method was used. First, the analyst identified 15 guideline merger & acquisition transactions in the busing industry. For each target company, the operating income and the value of the target company debt plus its equity (i.e., its business enterprise value, or BEV) were obtained. In this case, the BEV was provided by Securities Data Corp. (SDC), a firm specializing in providing financial data. Exhibit 3-3 presents the BEV, EBIT and EBIT pricing multiple of each of the target companies.

After a rigorous due diligence, we concluded that the guideline transactions' median pricing multiple was applicable to the subject...

To continue reading

Request your trial