CHAPTER 2 FINANCIAL DISTRESS IN THE OIL PATCH

| Jurisdiction | United States |

FINANCIAL DISTRESS IN THE OIL PATCH

Dorsey & Whitney LLP

Dallas, Texas

Mark L. Burghardt

Dorsey & Whitney LLP

Salt Lake City, Utah

[Page 2-1]

H. JOSEPH ACOSTA is a partner in the Bankruptcy & Financial Practice Group, in the Dallas office of Dorsey & Whitney LLP. Joseph has a broad base of bankruptcy, corporate restructuring and commercial litigation experience, having worked at national and international law firms for most of his career. During his 22+ years as a lawyer, he has been involved in some of the largest and most complex restructurings and litigation projects in the United States. He has taken lead roles in successfully representing debtors, banks, financing companies, distressed companies, committees, trustees, individuals, landlords, asset purchasers, retailers, and commercial creditors in all types of proceedings, including bankruptcy proceedings, federal and state lawsuits, arbitrations, and appeals.

MARK BURGHARDT, is a partner in the Energy and Natural Resources Practice Group, in the Salt Lake City office of Dorsey & Whitney LLP, where he represents clients in the energy and natural resource industry in litigation, administrative hearings, and transactions. Mark engages with clients to prevent and solve issues with the location and development of their oil, gas, mining, and renewable energy projects. He has worked with companies on projects involving federal, state, private, and Indian lands. Mark has also represented clients in a wide range of transactions and joint ventures. He has litigated energy development and land use disputes in both federal and state court and has routinely appeared before Utah Board of Oil, Gas and Mining and the Utah Division of Environmental Quality.

[Page 2-2]

SYNOPSIS

A. Introduction

B. Industry Participants

1. Key Players

2. E&P Companies

3. Midstream Companies

4. Downstream Companies

5. Oil Field Services Companies

C. Traditional Financing Sources

1. RBL Loans

2. Multi-Source Financing

3. Equity Capital

4. Commercial Loans

5. Acquisition Financing

6. Project Bonds

7. Expansion Financing

8. Hedging

D. Liquidity is a Necessity

1. Capital Intensive Industry

2. Liquidity Shortfall During Commodities Volatility

E. Prioritizing Obligations and Assets

1. Maintaining Leases

2. Contractual Obligations

F. Financing Issues in Bankruptcy

1. Working with Lenders/Avoiding Foreclosure

2. Fulcrum Debt Strategies

[Page 2-3]

3. Post-Bankruptcy Financing

4. Syndicated Loans

5. No Postpetition Financing

G. Conclusion

[Page 2-4]

A. Introduction

According to the U.S. Energy Information Administration (EIA), the United States (U.S.) regular gasoline retail price as of the Monday before Labor Day fell to $2.22 per gallon this year, the lowest level for this time of year since 2004.1 The EIA concludes that U.S. gasoline prices are relatively low because of continued low demand for gasoline since mid-March, when travel demand fell because of efforts to limit the spread of coronavirus.2 Indeed, monthly motor gasoline consumption in the U.S., measured as product supplied, reached a low of 5.85 million barrels per day during April 2020, the lowest level since 1974.3

There is little question that U.S. oil and gas production is expected to experience a decline in response to the first quarter's supply-and-demand shocks. In addition to reduced production of newly drilled wells corresponding to a reduction in drilling activity, oil and gas production naturally experiences declines in connection with the monetization of existing wells.4 Specifically, shale wells typically decline 70 to 90 percent relative to their peak production within a three-year period, with the large majority of that production decrease taking place within the first 12 months.5 Consequently, the absence of current drilling activity can rapidly result in the decrease of U.S. oil production. According to estimates developed by energy news website oilprice.com, the absence of drilling in U.S. shale basins would theoretically cause a decline in production by more than one third to less than 5.0 million barrels per day by the end of 2020.

There is also little surprise that there were almost 50 bankruptcies during the first half of 2020 among (a) 25 exploration and production (E&P) companies, (b) 19 oil field services (OFS) companies, and (c) 3 midstream companies.6 The numbers are continuing to increase during the second half of 2020, placing (as of August, 2020) a total of $70 billion of debt at risk among E&P and OFS companies. If West Texas Intermediary (WTI) continues to hover around $40/barrel, we could (a) witness another 29 more filings among E&P companies this year, adding another $26 billion of debt at risk, and (b) 150 or so filings during the next 2 years, representing another $128 billion in debt among E&P companies.

According to BDO's 12-Month Energy Investment Outlook, the pandemic has exacerbated these pressures, leading to even lower oil prices, sharp drops in demand, and a widespread economic downturn.7 Given the COVID-19 resurgences in certain states, and notwithstanding

[Page 2-5]

governmental assistance, the demand for oil will continue to be depressed, thereby leading to more bankruptcies on the horizon.8

Because the oil and gas industry is a capital-intensive industry, there are often issues with financing arrangements made with industry participants. In a distress scenario, these issues commonly relate to negotiating with lenders to cure defaults, developing strategies to maximize the value of assets, preserving the rights of secured parties, navigating through disputes amongst different tranches of debt or within a lender group, obtaining new take-out financing and, possibly, operating without no new financing. Addressing these and other financing issues are critical to the viability of an oil and gas company.

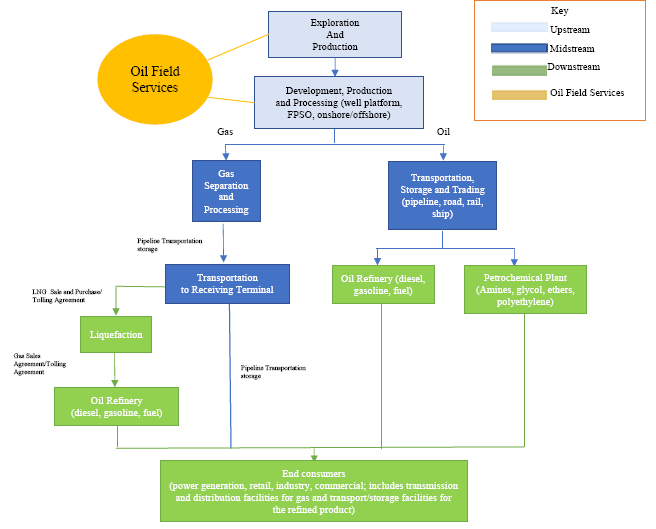

B. Industry Participants

1. Key Players

The four major types of oil and gas companies can be broken down in to 4 groups:

• Upstream companies or E&P companies;

• Midstream companies;

• Downstream companies; and

• OFS companies.

The chart below illustrates how each one operates:

[Page 2-6]

2. E&P Companies

E&P companies participate in the search for and the recovery and production of crude oil and natural gas.9 Activities within the upstream sector include searching for potential underground or underwater oil and gas fields, drilling exploratory wells, and drilling and operating wells that recover and bring to the surface crude oil, natural gas and related liquids.10

E&P companies' primary assets are their oil and gas reserves, which consist of the hydrocarbons below the surface that have not yet been produced and are economically viable to extract.11

[Page 2-7]

Reserves can be classified into two main categories: proved and unproved reserves. Proved reserves are quantities (volumes) of oil or natural gas that are recoverable in future years from known reservoirs under existing economic and operating conditions.12 Within the category of unproved reserves, probable reserves have a 50% probability that reserve quantities will be higher than estimated and a 50% probability that the reserves quantities will be lower than estimated.13 Possible reserves have a 10% probability that reserves quantities are higher than estimated and a 90% probability that reserves quantities will be lower than estimated.14

3. Midstream Companies

The midstream sector of the oil and gas industry comprises the transportation and processing of extracted hydrocarbon products from the upstream directly to the onshore market or to port facilities for storage or onward passage to the relevant domestic or international downstream market (or both). This sector comprises the construction, operation, and maintenance of pipeline projects and vessels, and the building of storage and processing facilities (or any combination of these).

U.S. Midstream companies are frequently incorporated as master limited partnerships ("MLPs"), which are publicly traded on a stock exchange qualifying under Section 7704 of the Internal Revenue Code.15 The vast majority of MLPs are pipeline businesses, which generally earn stable income from the transport of oil, gasoline, or natural gas. More specifically, energy MLPs are defined as those that own energy infrastructure — including pipelines, storage, terminals, or processing plants for natural gas, gasoline or oil — in the United States. MLPs' access to capital markets and low costs of capital on a pretax basis create a compelling valuation proposition in the transaction markets.

4. Downstream Companies

A downstream operation refers to those projects that process extracted resources to make them into a usable end product or a source of energy supply, including by way of power plants, refineries, LNG liquefaction and regasification facilities and petrochemical plants.

Although lower oil and gas commodity prices adversely impact the valuation of E&P companies, the valuation of downstream companies, such as refiners, often benefits from lower prices of the commodity feedstock.16 The crude oil of E&P companies is a primary feedstock for downstream companies, and lower feedstock prices may result in higher crack spreads for downstream companies. Crack spread is the differential between the price of crude oil and the price of petroleum products extracted from it — that is, the profit margin a refinery can expect when it "cracks" crude oil. As a result, in a low commodity price environment, downstream companies can be expected to benefit from higher crack spreads in the near term.

[Page 2-8]

5. Oil Field Services Companies

OFS companies provide the labor and equipment that E&P companies utilize during the various stages of development. There are different types of OFS companies, ranging from diversified companies that...

To continue reading

Request your trial