Bankruptcy in the Golden Years: the Case for Increasing Exemptions for Elderly Americans

| Publication year | 2023 |

| Citation | Vol. 39 No. 2 |

Bankruptcy in the Golden Years: The Case for Increasing Exemptions for Elderly Americans

Danny Fitzpatrick

This Comment analyzes 11 U.S.C. § 522(d) and several state exemption statutes for their success at providing elderly debtors sufficient exemptions to maintain their quality of life after filing for bankruptcy. Exemptions are assets that are excluded from an individual debtor's estate upon filing for bankruptcy and that serve as protection against creditors stripping the debtor of all pre-petition property interests. State and federal exemptions vary dramatically, with some states carving out additional exemptions specifically for elderly debtors. For example, states like Massachusetts and Maine recognize additional exemptions for elderly debtors with regards to their homesteads.

Bankruptcy filing rates for elderly Americans have increased while elderly debtors continue to receive inconsistent treatment in bankruptcy across various states. Accordingly, similarly situated debtors can face disparate outcomes based solely on their state of residence.

This Comment argues that Congress should follow the lead of states like Massachusetts and Maine by providing additional bankruptcy exemptions for all elderly Americans, because elderly debtors have different fundamental needs and goals from other American debtors. A revised federal exemption statute is the best approach for resolving the unequal state-by-state treatment of elderly debtors, as well as for meeting their unique bankruptcy needs.

[Page 446]

Introduction..........................................................................................447

I. Background ................................................................................ 449

A. The Changing Financial Landscape for Elderly Americans ..... 450II. How the Federal Government Can Create Sufficient Protection for Elderly Debtors...........................477

B. Overview of Exemptions and the Fresh Start Doctrine ............ 453

1. The Role of Exemptions in Chapter 7 and Chapter 13 Bankruptcy Filings ............................................................ 455C. Specific Federal Exemptions Under 11 U.S.C. § 522 ............... 457

2. The Fresh Start Policy ...................................................... 456

1. The Federal Exemption for Home Equity........................... 458D. Representative State Exemptions ............................................. 465

2. The Federal Exemption for a Motor Vehicle ...................... 460

3. Federal Exemptions for Retirement Income ....................... 461

4. Social Security and Bankruptcy......................................... 463

5. Other Federal Exemptions ................................................ 465

1. The Constitutionality of State Exemptions ......................... 466

2. Exemptions in Texas ......................................................... 469

3. Exemptions in Florida ....................................................... 471

4. Exemptions in Massachusetts ............................................ 472

5. Exemptions in Maine ......................................................... 474

A. Model Act vs. Federal Legislation ........................................... 478

B. Equal Protection Concerns with Unequal Treatment of Elderly Debtors ...................................................................... 478

Conclusion.............................................................................................480

[Page 447]

Elderly Americans are filing bankruptcy at higher rates than ever, both in terms of the number of cases filed and as a share of total bankruptcy petitions filed.1 Filing for bankruptcy used to be predominantly for younger Americans struggling to find stability in early adulthood; however, Americans between the ages of sixty-five and seventy-four are now filing at approximately the same rate as Americans aged twenty-five to thirty-four.2 Recently, elderly Americans have caught up to other age groups and, as of August 2021, Americans over sixty years old account for 23.41% of bankruptcy filings, though they make up approximately 22.64% of the population.3 Accordingly, modern issues with managing debt are just as much of a concern for elderly Americans as they are for younger Americans.

Increases in debt levels for elderly Americans would not be as significant of an issue if their increased debt levels were offset by increasing sources of income to pay off creditors. For example, even though corporations and governments continue to increase their debt levels over time, they have largely been able to pay their increased debt through increased productivity and investments.4 For older individual debtors, however, their reliance on fixed income streams and their difficulty in generating new income combine to exacerbate the issue of growing debt levels. As James Frego and Glen Turpening point out, "[b]ankruptcy is becoming a bigger part of the social safety net for senior citizens where the old system of a secure, lifelong income is being replaced by permanent debt relief."5

One factor increasing the amount of older debtors filing for bankruptcy is simply the number of elderly households with outstanding debt obligations.6 Of households headed by individuals aged sixty-five and over, 61.1% held debt in

[Page 448]

2016 as compared with 37.8% of households in that demographic in 1989.7 Not only are more elderly households in debt, those elderly households that do carry debt continue, on average, to carry more debt.8 More elderly Americans are taking out debt and they are taking out more of it, increasing their likelihood of insolvency.9

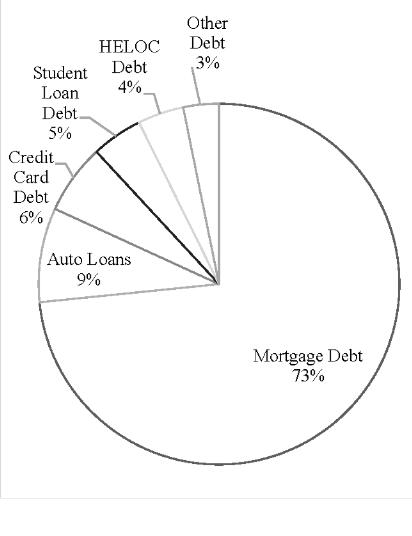

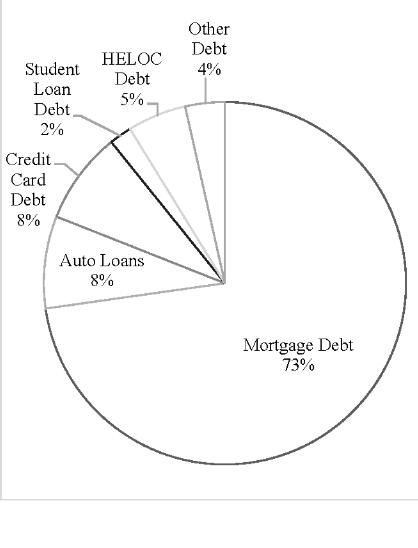

The composition of debt for older debtors shows the types of debt they have the most difficulty repaying. As of the third quarter of 2021, for Americans between ages sixty and sixty-nine, 73.39% of their debt was mortgage debt, 8.45% of their debt was in auto loans, 6.27% of their debt was credit card debt, 4.58% was student loan debt, 4.12% of their debt was in home equity line of credit ("HELOC") debt, and 3.19% of their debt was other debt.10 For Americans over seventy, 73.05% of their debt was mortgage debt, 8.26% of their debt was in auto loans, 8.26% was credit card debt, 5.28% was HELOC debt, 2.01% was student loan debt, and 3.54% was other debt.11 Mortgage, auto loans, and credit card debt represent huge burdens for the average older debtor.

[Page 449]

This Comment discusses: (1) the changing financial landscape for elderly Americans, (2) an overview of exemptions and the fresh start doctrine, (3) specific federal exemptions under 11 U.S.C. § 522, (4) representative state exemptions, and (5) how the federal government can create sufficient protection for elderly debtors via amendment to the Bankruptcy Code. This Comment shows that the fresh start promised by bankruptcy is not as attainable for elderly debtors, who often have limited fixed incomes and decreased earning potential, as it is for other similarly situated debtors. To close this gap, the federal government should follow the lead of Massachusetts and Maine and expand upon its exemption schemes to create more generous exemptions for elderly debtors filing for bankruptcy.

The rise and fall of financial safety nets in the United States helps explain elderly Americans' dependence on bankruptcy as a remedy. Bankruptcy scholars Deborah Thorne, Pamela Foohey, Robert M. Lawless, and Katherine Porter discuss the history of America's treatment of the elderly, writing, "[w]ith the emergence of neoliberalism in the early 1980s, portions of the social safety net that many retired Americans depended on, namely retirement savings and affordable health care, weakened, and the responsibilities for and costs of were shifted to individuals."12 For individual debtors in the twenty-first century, some of the primary reasons for bankruptcy filings include rising healthcare costs and insufficient income during retirement.13 In a presentation given to the American Bankruptcy Institute, Kenneth L. Gross explained six of the main drivers of elder bankruptcies as

(1) the elimination or reduction of equity in homes due to the financial crisis; (2) the increase of student loan debt among the elderly; (3) the historical rise of credit card debt; (4) social security increases that do not keep pace with inflation for the elderly; (5) overcoming of the "stigma" the elderly often placed on filing; and (6) plain old need.14

[Page 450]

A. The Changing Financial Landscape for Elderly Americans

A combination of social movements and changes in federal legislation allowed many retirees in the late twentieth century to retire comfortably.15 Some of these changes in American society included the passing of the Social Security Act of 1935, the introduction of Medicare and Medicaid in 1965, and private and public employers' provision of defined benefit pension plans to employees.16 Furthermore, early on after the passage of the Social Security Act, the retirement age for full social security benefits was sixty-five, and Americans on average could expect social security payments to provide 40% of their preretirement income.17

Recently, the estimated average social security retirement benefit in May 2022 was $1,668 a month,18 which works out to an expected annual benefit of $20,016. This is noticeably smaller than the annual income of the median working American male in 2020, which is $67,304, and that of the median working American female, which is $49,214.19 Even though social security income is expected to be only a fraction of working income, as of 2018, a large portion of retirees rely on social security for 90% or more of their monthly income.20 The lack of retirement income savings plus...

To continue reading

Request your trial